Click Here for a Printable Copy

Clients and Friends,

There has been significant market volatility and disruption over the course of the last week after the long-awaited revealing of the Trump administration’s tariff plan. While the managed portfolios that form the core of our investment strategies have held up well, we do plan to rebalance those portfolios, while making the following changes moving forward:

- We understand that volatility can be unsettling. Our team is committed to helping you navigate these uncertain times by staying focused on a long-term, disciplined investment process. This process is designed not only to preserve capital during periods of market stress, but also to position portfolios to benefit as the economic landscape evolves.

- Due to the possibility of lower interest rates and a potential recession as tariffs impact the economy, we are liquidating our bank loan position, and reallocating to lower risk bond portfolio investments.

The factor-based investments will be liquidated for tax loss harvesting purposes. In addition, we don’t believe these rules-based funds with limited rebalancing opportunities will react well during such a dynamic period in the markets with so much uncertainty. - We are reallocating those funds to more value-oriented and thematic investments. We believe these investments have less expensive valuations, higher dividend and dividend growth profiles, and will better weather possible economic turbulence.

Macroeconomic Update:

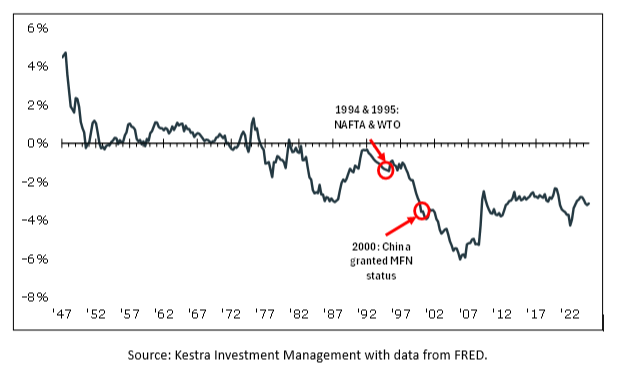

As we noted in a post late last week, US trade policy has been focused on prioritizing free trade, and its associated benefits, for the last half century, highlighted by the creation of the North American Free Trade Agreement (NAFTA) and the World Trade Organization (WTO) in the mid-1990s, and by granting China most favored nation status and their admission to the World Trade Organization in the early 2000s. Increasing free trade brought with it access to cheap goods and a fast-growing economy. Supply chains were increasingly moved overseas, to take advantage primarily of cheap labor, as well as lower cost of capital and other operational efficiencies which were many times subsidized by foreign governments. As may be seen below, this also resulted in the United States moving from a trade surplus to a trade deficit over time:

For the last decade, there has been an increasing emphasis on and analysis of the costs associated with this free trade, which include the hollowing out of America’s manufacturing base and the related loss of jobs, as well as supply chain vulnerabilities. This second issue was particularly highlighted during COVID, when the US population quickly realized that many key goods, including computer chips and pharmaceuticals, that our society relies upon are in fact not manufactured onshore.

Concurrently with the expansion of free trade, the US has also been on an unsustainable fiscal path. At present, the U.S. national debt is just over $36.5 trillion, with estimated federal budget deficits of over $2 trillion per year adding to that total. While historically, defense, healthcare (Medicare/Medicaid), and Social Security made up the largest majority of federal government spending, interest payments on the federal debt may reach over 18% as a share of federal revenues by the end of 2025, representing a fourth major spending category and quickly adding to the overall debt level itself.

One of the tools that the Trump administration has decided to use to attempt to rectify and renegotiate the current landscape is tariffs. Last Wednesday, the President announced a baseline 10% tariff for all imports, regardless of the country of origin. The administration also announced much higher tariffs for sixty countries where they view the relationship as the most imbalanced, including China which can be put in its own bucket with total tariff levies now approaching 64%.

We view most of these tariffs other than China’s as starting points for bilateral trade negotiations, and as anyone who has ever negotiated anything knows, you ask for a lot at the beginning of a negotiation so that, when you reach a negotiated resolution, you end up getting most of what you want.

That being said, we believe that the communication concerning these tariffs, and their timing and planned implementation strategy, was extremely poor. The result has been confusion and a lack of clarity as to the effect this will have on global growth and inflation. Stock markets in general hate uncertainty, translating to the roughly 10% decline that the S&P 500 experienced during the two trading days following the tariff announcement; the Russell 2000 and the Nasdaq 100 fell by more.

We will get to an analysis of our core portfolios, and our thoughts on investing alongside these tariffs, in a minute. First, we want to acknowledge that the size and abruptness of these changes is uncomfortable to markets, and therefore to portfolios. That being said, here are a few thoughts to help stay calm during these turbulent times:

- There were notable exclusions to the reciprocal tariffs, which include steel, aluminum, autos and auto parts, copper, pharmaceuticals, semiconductors, lumber, bullion, and energy and certain minerals that are not available domestically. While this of course did not get much if any coverage from traditional news outlets, we take it as a sign that there is some pragmatism and actual thought being given to the overall effect that the tariffs will have.

- Previous to this announcement, 25% tariffs were imposed on Mexico and Canada for non-USMCA (the successor to NAFTA) made goods. No further announcements regarding Mexico and Canada were made last week. We believe that the implication is that goods that continue to be made in compliance with the previously negotiated USMCA trade agreement will continue not be tariffed in accordance with that agreement. We believe that this is an important signal to the countries that will be on the other end of future bilateral trade negotiations with the US.

- Using Nike as a short-term example, we believe that the most prudent path forward for portfolios may in fact be patience. On Thursday, April 3rd, one day after the tariffs were announced, Nike stock fell over 14% on the news that imports from Vietnam, where Nike makes 50% of its footwear and 28% of its apparel, would be tariffed at a 46% rate. The following day, Nike promptly rose 3% (on a day when the overall market was down over 5%) on news that the Vietnamese government had already reached out to the Trump administration to negotiate a new trade agreement. This was confirmed by a letter from the Vietnamese party chief over the weekend.

While we obviously have no crystal ball, we would note that Kevin Hassett, the current director of the National Economic Council at the White House, stated over the weekend that over 50 countries have reached out to the U.S. to begin trade negotiations. While we have no definitive idea as to which countries those are, and the relative importance to the global economy, we are simply acknowledging that successful bilateral trade negotiations can reverse the current situation very swiftly.

Core Portfolio Review:

While the long-term goal of these policies is to strengthen the US economy and fiscal position, in the short run they may end up increasing inflation and lowering economic growth, a condition otherwise known in economic terms as stagflation. As you know, our core portfolios are well-diversified, built to withstand possible market shocks, which typically come without warning. It is also important to recognize that tariffs don’t impact all companies and areas of the stock market in the same way. While you will undoubtedly hear about the negative impacts of tariffs, it is also true that some assets will benefit. As an example, our infrastructure investment is up over 3% so far this year. In addition, recent dollar weakness, which is rare during market stress, could mean that investors are shifting investments away from the US, and towards foreign markets, which would benefit our international investments.

In addition, there are a number of factors that could buffer any additional downside for stocks. First, the federal government will now turn to working on a large tax cut and regulatory reform, both of which could help to soften the shock the economic growth. Second, the market is already down substantially, with the median stock in the Russell 3000 down 38% from its October highs1, and the NASDAQ having peaked with the introduction of the Chinese DeepSeek AI technology back in January. Both of these statistics point to the fact that the markets were very concentrated for the past year, mainly led higher by the “Magnificent 7”, which are now reversing and leading the way lower towards more reasonable valuations.

That being said, given the increased probability of stagflation, we are going to rebalance our core portfolios, while making the following changes to align them with what may be a slow-growth environment for the foreseeable future:

- On a year-to-date basis, all of our bond investments have risen except for our bank loan fund, which is slightly negative. While this primarily shows the beneficial impact of diversification and the ballast that bonds provide to a balanced portfolio, we do think that there is a chance that we enter a recession, and that interest rates will decline. If that were to happen, the riskiest portion of the bond portfolio are the bank loans. At the moment, we are more focused on preservation of capital than possibly earning a few more percentage points of interest, and as such, we are reallocating that bank loan position back to the rest of our bond portfolio that has been chosen for its safety and security.

- We are also going to tax loss harvest the three factor funds that we had invested in, including a momentum factor fund, a quality factor fund, and a dynamic factor rotation fund, and reinvest in a combination of more value-oriented funds already in the core portfolios. Harvesting tax losses when available for use to offset gains and other income on your tax returns next year always makes sense. Beyond that, while these funds are structured to take advantage of certain market factors, we believe that the current level of uncertainty associated with the potential impact of tariffs on different businesses and industries, and the quickly changing dynamics, means that rules-based factor funds that only rebalance quarterly or semi-annually may be caught having invested in portions of the market that may on the wrong side of the tariff discussions. We will reallocate those funds back to more value-oriented and long-term thematic investments, which we believe will hold up well as the economy and markets digest the impact of these tariffs, and the possible new global trading order, on inflation, global growth, and earnings going forward.

As difficult and unsettling as change and market turbulence can be, as always, we encourage you to stick with your long-term, strategic investment portfolio. Long-term investors have consistently been handsomely rewarded over time.

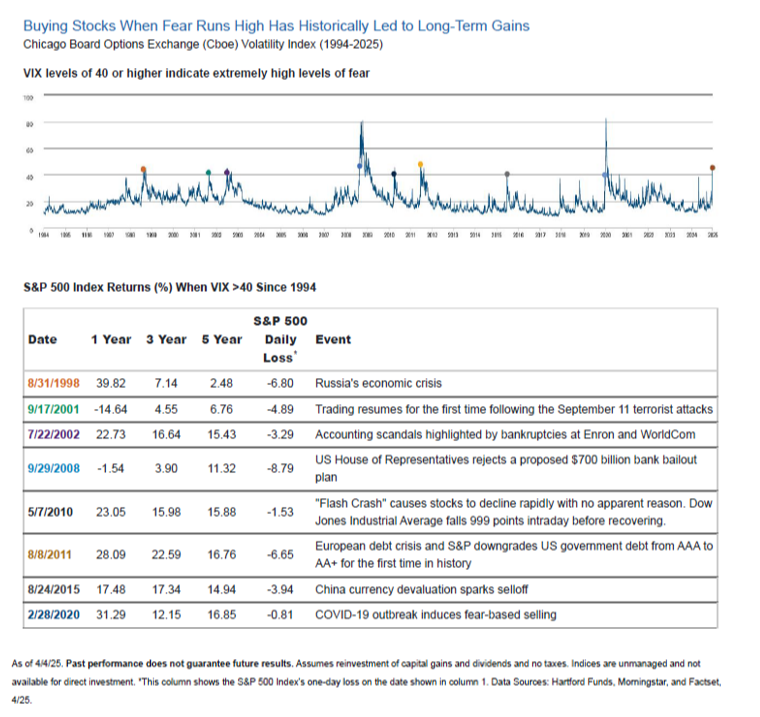

For example, the Cboe VIX index measures market volatility. It is often referred to as the “fear index” because it gauges the market’s expectation of 30-day volatility. On average, the VIX measures about 20, but may spike during periods of high fear.

Historically, when the VIX has spiked above 40, market declines sustained during those periods have been recovered within a few years, along with additional returns as may be seen below:

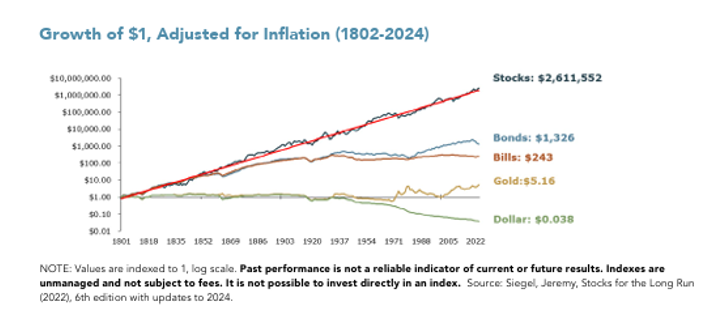

Market pullbacks are a normal part of investing, and as just illustrated, even the most significant may also prove temporary. At the end of the day, while they may be very volatile from time to time, stocks are the most stable in the long run:

As always, if you have any questions, or would like to speak to a member of our team regarding your portfolio, please do not hesitate to give us a call.

Kindred Wealth Partners

Footnotes

1 – Carter Worth, CNBC Fast Money, April 4, 2025

Disclosure:

A diversified portfolio does not assure a gain or prevent a loss in a declining market. There is no guarantee that any investment strategy will be successful or will achieve their stated investment objective.